Discussions of internal corporate prediction markets have sometimes pointed out that open, anonymous participation can lead to better information flow within the corporation. See, for example, Jed Christiansen’s write-up of the recent Consensus Point conference, particularly his notes on the presentations of Dave Perry and Fortune Elkins.

A lot of business research has been devoted to the topic of communication within an organization. An article from HBS Working Knowledge tries to sum up the current state of research into roadblocks to communication within an organization.

This propensity to maintain silence, a flaw at once personal and organizational, is “-widespread and problematic”- in both the public and the private sectors, says HBS professor Amy Edmondson, who chairs the Doctoral Programs and teaches in the Technology and Operations Management unit.

“-To cite one example, former HBS doctoral student Jim Detert and I interviewed some 200 people of all ranks and functions in a high-tech multinational. We found to a very significant degree that people did not speak up about things they deemed important. Most of those were not ‘-bad news’- things- to our surprise we found that people were reluctant to voice what they perceived to be good ideas, unless they were extraordinarily confident they would be well-received. And this in a firm that lives and dies by its ideas.”-

Edmondson says this reluctance to speak up stems variously from fears that superiors will not like the idea or that it may appear to criticize the status quo, which most people find reassuringly familiar or dangerous to challenge. Edmondson sums up the mental calculation this way: “-The potential costs to me for speaking out seem reasonably certain and somewhat immediate- the potential benefit to me for speaking out seems rather uncertain and definitely long-range.”-

The article cites HBS professor Max Bazerman to the effect that “within organizations, candor should be rewarded and incentives designed to encourage [it],” though the article does little to elaborate on the idea.

Instead, the article urges business executives to “develop disagreement” and suggests installing “a team at the top where high contention is demanded and rewarded.” During decision-making processes, according to one professor quoted, executives should ask probing questions and insist that managers “present each situation in objective terms, rather than with a positive spin.” The article sums up with, “What’-s required in an organization is honest, thorough, and ongoing self-criticism, which, after all, is at the heart of continuous improvement.”

Part of the problem with the article is that it is exactly the old-style managerial approach that apparently doesn’t work. For how many decades have business executives been told to encourage honest disagreement, to reward challenges to the status quo? Saying “challenge the status quo” is the status quo. If it worked, then information would already always flow smoothly within corporations.

When the thing that stops an employee from speaking up is a mental decision calculus that compares relatively certain and immediate costs to uncertain future gains, as described by Edmonson, “demanding and rewarding high contention” just seems to raise the stakes. Raising the stakes seems like it would be counter-productive.

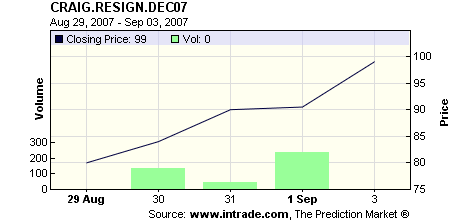

Maybe contentious meetings aren’t a good approach for eliciting honest revelations. So if what is said about prediction markets is true – if they can help information be gathered and processed in cases in which traditional ways of gathering and processing information fail – then they can be wonderful things. What was the example that Christiansen cited (from Perry’s presentation), a “forecasting team was trading against their official forecast”? That example shows information flowing more smoothly through prediction markets than through traditional channels.

The article hints at some of the reasons that prediction markets can improve information flow. With private, anonymous trading, the choice to disclose information via the market dramatically revises the mental decision calculus involved. The trader is rewarded if right and penalized if wrong, but in either case the disclosure and net reward is a private matter rather than social event. (At least until you brag about it around the water cooler.)

As the article said, candor should be rewarded and incentives designed to encourage it. Prediction markets provide incentives for candor. Not only that, but over time the traders with useful candor are encouraged by accumulated gains, while blowhards find their accounts diminished.

It is true that prediction market prices present relatively limited signals. Prices may go up or down, but they never say why. But with a signal, at least someone knows to start asking “why” and that is better than not knowing.

[Cross posted at Knowledge Problem.]