![]()

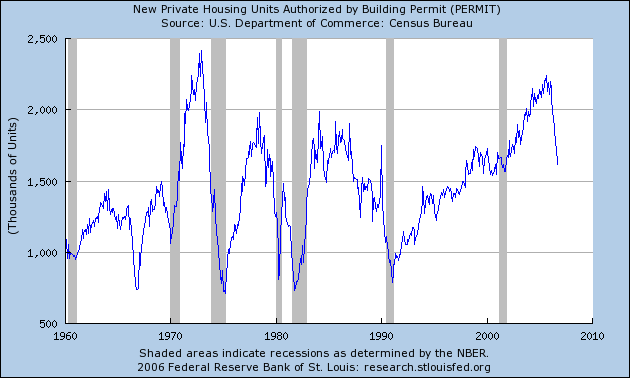

Something for everyone in this week’-s data on housing from the Census Bureau. Pessimists will note the alarming 6% plunge during the month of September in seasonally adjusted new building permits. That one-month drop from the already low levels of August leaves them down 28% from September 2005. News this week of rising delinquencies and foreclosures provides more fuel for the pessimists’- fire.

|

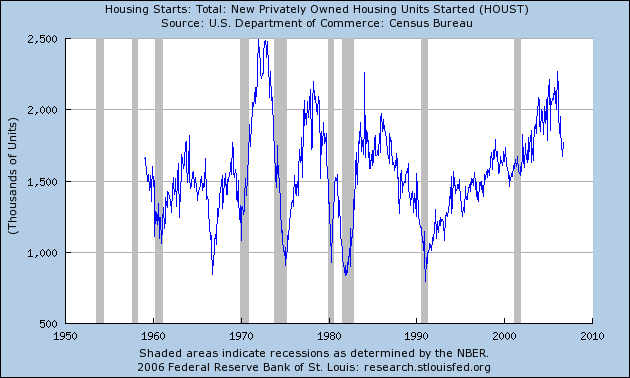

Optimists, on the other hand, might see new evidence that the housing bottom has been reached in the encouraging move in the number of new housing units started. This was up 6% from August to September, though still down 18% year to year:

|

For those of us who were unsure before this week, we’-re stuck in the same rut at the end of the week. The effect of this summer’-s drop in mortgage rates should start to show up in next month’-s home sales, and we’-ll have to wait to see if that effect is sufficient to outweigh the possible dynamics from financial distress and rapidly changing expectations.

The optimists seem to be winning the argument as far as commodity markets are concerned. Commodity prices had been battered down as the dismal housing data came in during September. But over the last two weeks, copper, zinc, and aluminum have surged back up dramatically. It may be that the only way these prices will be kept in check is if GDP growth stays below 2% for the coming year.

And although the headline CPI showed a dramatic 0.5% drop within the month of September alone, Dave Altig is none too impressed, noting that more robust measures such as the median CPI are still up 3.5% year-to-year:

|

Mixed (as opposed to really bad) news for housing and “-unwelcome”- news on core inflation have eroded the likelihood that we will see the Fed cut interest rates by spring. Here’-s the recent behavior of the March 2007 fed funds futures contract (subtract from 100 to get the implied interest rate):

|

At the start of this month, traders had been betting on a 5.0% rate (a cut of 25 basis points from the current value) by March. Those hopes have now evaporated, with the current consensus for a prediction of no change.

I’-m wondering though whether “-no change”- might be the least likely outcome at this point. If we start to see some serious financial repercussions develop in housing, I’-d look for a rate cut, and wouldn’-t worry in that event about commodity prices, since I would expect to see commodities fall sharply on news of a big downturn in economic activity. On the other hand, if instead we have seen the bottom for housing and the core inflation numbers remain this high, I’-d look for the Fed to tighten further.

Either way, you might want to exercise some caution before thinking you’-ll pick up some homebuilder equities at these bargain prices.