![]()

Since Halloween, financial markets seem to be getting spooked again.

Larry Kudlow writes:

Until recently, I thought the Fed could stand pat at their December 11th meeting. However, I have completely changed my mind in light of the continuing credit market turbulence.

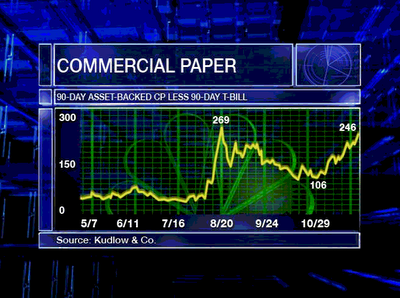

Kudlow notes that the spread between 30-day asset-backed commercial paper and U.S. Treasuries, which spiked up dramatically after August’-s liquidity events but subsequently eased back down, climbed back up during November to the neighborhood of its previous high.

|

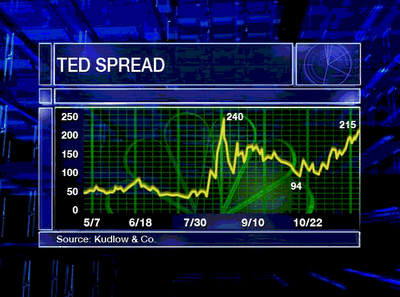

The same is true of the spread between the London interbank offered rate and Treasuries.

|

One of the features of the initial financial turmoil on which I commented last August is that it seemed to be confined specifically to the financing of problematic securities, but was not showing up as a broader risk premium in something like the spread between Baa-rated corporate bonds and 10-year Treasuries. But the latter spread has made a significant move up over the last month, and now stands 80 basis points higher than in July.

|

A sharp upward move in the Baa-Treasury spread is often associated with the early stages of an economic downturn, as the following longer-term perspective using monthly data illustrates:

|

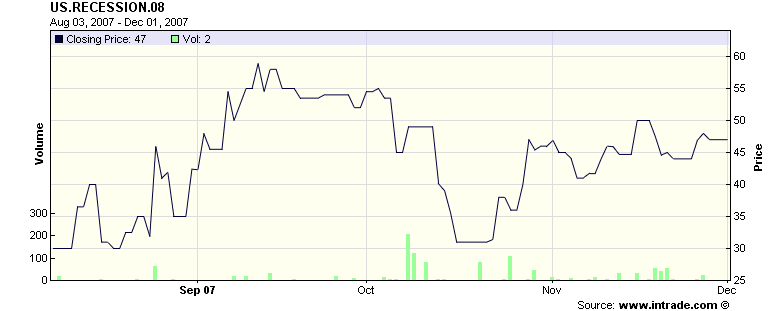

For what it’-s worth, bettors at Intrade also seem to believe that the risk of a U.S. recession during 2008 has crept up since mid-October.

|

Cross-posted from Econbrowser.